First Time Homebuyers

First Time Homebuyers in La Crosse WI | Step by Step guide to Buying your First Home

A simple, honest guide to buying your first home in the Coulee Region—with someone who’s got your back.

First Time Homebuyers

A simple, honest guide to buying your first home in the Coulee Region—with someone who’s got your back.

Let’s simplify this. Here’s what it actually looks like to buy a home in today’s market:

This is your starting point.

A lender will:

👉 Bonus: Julie has trusted local lenders in La Crosse County, Winona County, and surrounding areas she can connect you with.

We’ll help you figure out:

This is where Julie’s “perfectly imperfect” approach shines—she’ll tell you the truth, not just what you want to hear.

This is the fun part.

You’ll:

👉 And yes… the first house you see probably won’t be “the one.” Totally normal.

This is where strategy matters.

Julie will help you:

In competitive markets like La Crosse and Onalaska, this step can make or break the deal.

I wrote a great blog post on how to write a competitive offer!

Once accepted:

👉 Even in competitive situations, you still have options to protect yourself.

You sign paperwork, get the keys, and officially become a homeowner.

Yes—it’s a lot of signatures. No—you don’t need to understand every legal term. That’s what Julie is here for.

Here's a blog post discussing more details about your closing day.

This is where things feel different.

Julie isn’t here to “sell you a house.”

She’s here to:

She brings:

No pressure. No scripts. Just honest advice and a plan that fits you.

And yes… probably a few laughs along the way.

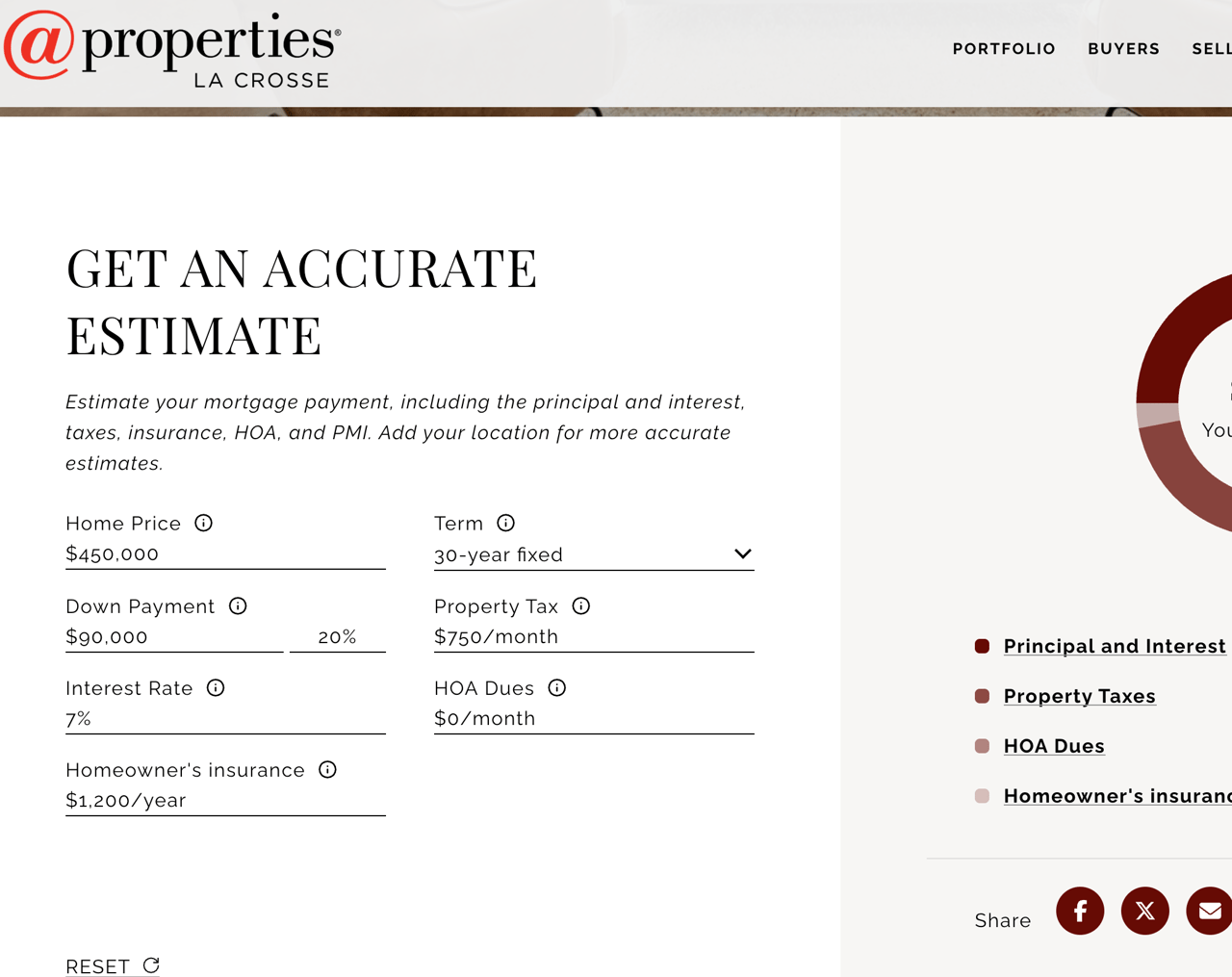

Let’s clear up the biggest myth: You do NOT need 20% down payment. Many first-time buyers in the Coulee Region purchase homes with: 3% – 5% down (Conventional loans), 3.5% down (FHA loans), 0% down (VA or USDA, if eligible). There are some other costs you can expect: Closing costs (typically 2–4%), inspection, appraisal, moving expenses. But don't stress about those; there is always a way. The good news? There are programs in Wisconsin and Minnesota that can help with down payment assistance. For more information on your mortgage options, please review our blog post on Financing here!

FHA Loans are great options for first time home buyers. They typically have lower credit score requirements, can only require down payments as low as 3.5%, and are specifically designed to provide low cost of entry into buying your first home.

Conventional loans, depending on programs offered by different financial institutions, can require as little as 3% down and provide long term cost savings.

Typically available for former or current service members and their immediate families, VA Loans can provide a low cost of entry to home ownership, including down payments as low as 0% and lower interest rates.

These loans are geographically specific and can be used when buying a home in rural areas. These can include many areas in our region, particularly Trempealeau, Monroe, Vernon, and Juneau Counties in Wisconsin. These typically have low cost of entry into home ownership including 0% down payments and lower interest rates.

Programs like WHEDA (Wisconsin) and Minnesota Housing can provide down payment assistance, reduced interest rates and other first time buyer incentives.

Best Way to get started? get in touch with me.

Here’s where a little guidance goes a long way:

Julie’s job? Make sure none of these happen to you.

Each area has its own personality:

Julie works across:

That local knowledge helps you:

Here are some quick answers to some common questions:

Most buyers put down 3%–5%. Some qualify for 0% down programs.

Yes—this is step one. It saves time and makes your offer stronger.

Yes. Lenders look at your overall debt-to-income ratio, not just one factor.

Yes—programs like WHEDA offer assistance and incentives.

No. Many loan programs allow for less-than-perfect credit.

Typically 30–60 days once you have an accepted offer.

In most cases, the seller covers buyer agent compensation—but this can vary. Julie will walk you through it clearly.

Julie was the perfect realtor for us as we navigated our first homebuying experience. She truly went above and beyond to make what could have been an overwhelming process feel manageable and did it all with so much kindness and plenty of laughs along the way! She was incredibly patient and always took the time to explain every step in a way that made sense to us. We had lots of questions and she made us feel heard every time. She was prompt in her responses and handled every twist and turn with professionalism and guided us through each challenge with confidence. Julie genuinely cared about our experience and made sure we felt comfortable, informed, and happy with every decision we made. We are so grateful for her support and would wholeheartedly recommend her to anyone, especially first-time buyers!

Julie is a pitbull who won't give up until she succeeds in marketing, selling, and closing a home. She is incredibly creative when it comes to marketing ideas, promotions, and dealing with buyer questions and concerns. If she doesn't know the answer, she'll investigate and get help from her team members until you're satisfied with the information. She was accessible at all times, returned every phone call or text message, and went above and beyond with her time and help just before closing when a last-minute problem cropped up. You couldn't be in better, more capable, more focused, and more committed hands!

Julie was friendly and very prompt with all communications. She helped me find just the right house in a safe neighborhood. She answered all my questions and got answers when she didn't know. She also sold my home while I was in the middle of a divorce, and she worked with my soon-to-be ex and me very professionally and didn't let our emotions take away from the mission of getting our house sold. She played middleman not just between us and another agent and buyer, but also between us to help us get the best price possible.

Julie was an absolute delight to work with. I would highly recommend working with her if you're looking for a realtor who not only listens to your wants and needs in a home, but also cares about them. She is very knowledgeable about the local area and can give you the rundown on basically any block in the city. Trust me, she has either lived there or knows someone who does. Julie made this process not only easier, but also enjoyable in a market that is absolutely not friendly towards buyers right now. Don't sleep on this one. She's the real deal!

Julie was amazing. Besides being professional in every aspect of my home search to purchase, she was attentive in my needs as a home buyer. She had the answers before I had the questions. She was committed to helping me find the perfect home. What I appreciated most about Julie is how she made me feel like I was not just a client but a friend. I never had to wait very long for replies and her commitment to her profession is stellar.

It was a privilege and pleasure working with Julie Delap. She's very personable, knowledgeable and has great communication skills. She understood our needs and budget and worked hard to find us the ideal home. I would definitely recommend Julie to other buyers.

Julie was wonderful! As first time home buyers she was a great advocate and explained everything to us step by step. She also helped make recommendations about lenders, inspectors, and more!

Julie was wonderful. She explained things in a client friendly manner, so clients understand and are protected. She promptly responded to questions and concerns. We received an offer right after the house was listed. Julie kept in close contact with the other agent and kept us updated. She continued to market our house yet be respectful to the offer and potential buyers. She is very friendly and personal. I would highly recommend Julie!

Julie was wonderful helping out family find the perfect house. She made the process of first home buyer experience so smooth and answered all of our questions. She will be my first contact in the future if we ever decide to sell or buy again.

As first-time homebuyers, we couldn’t have asked for a better realtor than Julie. She made the entire process smooth, stress-free, and even fun! Julie was knowledgeable, patient, and always quick to answer our questions. Thanks to her guidance, we found the perfect first home and felt supported every step of the way. Highly recommend!

Julie is great to work with! She has wonderful attention to detail when viewing properties and gives her honest opinion on condition items. She is always willing to go above and beyond. We have used her services as both sellers and buyers and will continue to use her for real estate transactions moving forward. Thanks Julie!

We couldn’t have bought our first home without Julie! From answering all the questions, calming the first time buyer nerves, to finding the perfect place, she can do it all. I will absolutely work with her in the future and recommend her to all family & friends.